You are now leaving our website and entering a third-party website over which we have no control.

Factors affecting life insurance premiums

You may have a rough idea of how much life insurance can cost. However, when it comes to understanding life insurance in Canada, not everyone may be as familiar with the different factors considered by insurers when determining life insurance premiums.

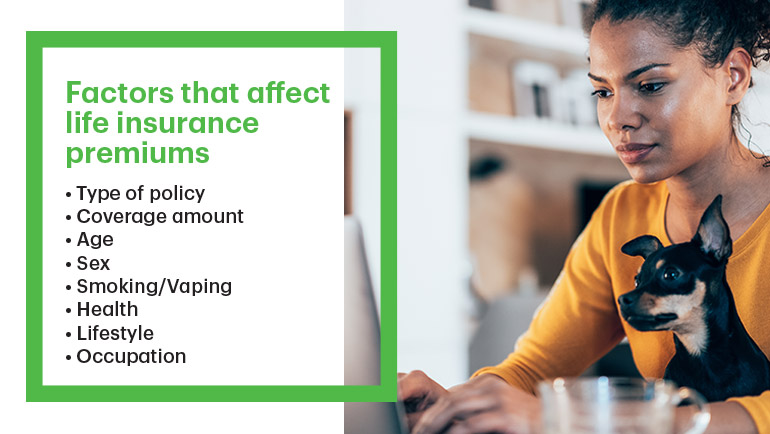

Factors like age, sex, smoking status, health, and lifestyle can all impact your life insurance premium. While it's important to find life insurance coverage that fits within your budget, there are other things you should consider as well, like seeking out a reputable life insurance company, learning about the different types of life insurance plans available to you, and understanding your unique life insurance needs at different life stages.

When you purchase a life insurance policy, the premium is the amount of money that you pay regularly (monthly or annually) to the life insurance company for your coverage.

7 common factors that could affect your life insurance premiums in Canada:

1. Age

How does age impact life insurance? Generally, when you're younger and healthier, you may pay a lower premium. When it comes to life insurance for seniors, there is a greater risk of health-related issues, which results in higher premiums. Applying for life insurance at a younger age could help you save money as you could pay lower life insurance premiums and potentially avoid medical exams.

2. Sex assigned at birth

Males typically pay higher premiums for life insurance than females because statistically, males have a shorter life span. In Canada, the average life expectancy is around 79.4 years for males and 83.8 for females1.

3. Health

You may have to undergo a health assessment as part of the life insurance application process. Depending on the information you provide in your application, this could include your family health history, a medical exam with a healthcare professional, and sometimes a review of your medical records.

You may pay more if you have certain pre-existing health conditions or illnesses. That said, addressing controllable health conditions can help you manage your premiums.

4. Smoking or vaping

Insurance companies charge you a higher premium if you smoke as smoking affects a person's health and lifespan. Generally, an individual who uses any substance or product containing nicotine is considered a smoker. Premiums could be more than double for a smoker. However, if you are a smoker when you purchase an insurance plan but quit smoking later, you may become eligible for non-smoker rates from your provider.

5. Lifestyle and occupation

If your hobbies include high-risk activities like motorsport and skydiving, you may need to pay more to offset the additional risk taken on by the insurer. Working in an industry with a lot of occupational hazards could also result in an increased cost.

6. Life insurance coverage amount

It's important to note that the higher the coverage amount you select, the higher your premiums will be. This is because the insurer is taking on more risk with a larger potential death benefit payout. When looking into coverage, you can use a life insurance calculator. At TD Insurance, the TD Life Insurance Calculator can help you estimate the amount of term life coverage that may be right for you.

7. Life insurance plans

When it comes to life insurance, the type of plan you select will impact your premiums. There are different types of plans that can meet your needs, so it's important that you do your research. At TD Insurance, we offer TD Term Life Insurance plans and TD Guaranteed Acceptance Life Insurance.

For all term life insurance plans, as the duration of the term increases, so does the cost. For example, a TD 10-Year Term Life Insurance plan costs less than a 20-Year TD Term Life Insurance plan which costs less than TD Term-100 Lifetime Coverage. TD Guaranteed Acceptance Life Insurance is for Canadian residents between the ages of 50 and 752, and you will be instantly approved for coverage ranging from $5,000 to $25,000 — regardless of your current health or medical history.

How much does life insurance cost?

Here's an example of how much life insurance could cost: Dan is a 30-year-old non-smoking male in good health, living in Canada. He is interested in and eligible for a term life insurance plan.

Dan is a homeowner with a $225,000 mortgage, no other debts, and an income of $50,000 per year. His parents, now retired, also live with him.

After reviewing the factors above, Dan applies online for $250,000 in coverage for a TD 10-Year Term Life Insurance plan. This amount could cover 100% of his mortgage if he passed away and provide some financial support for his parents (beneficiaries).

After receiving a 10% discount for applying online, Dan would pay $16.20/month3,4.

How much is $250,000 of term life insurance per month in Canada with TD Insurance? As a non-smoker, in good health, you could pay the following monthly premiums with a 10% discount if you are a TD customer5 or apply online3.

|

TD 10-Year Term Life6 |

TD 20-Year Term Life6 |

TD 100-Year Term Life6 |

20-Year-Old Male |

$16.20 |

$18.90 |

$185.00 |

20-Year-Old Female |

$11.70 |

$15.30 |

$185.00 |

|

|||

30-Year-Old Male |

$16.20 |

$19.80 |

$233.00 |

30-Year-Old Female |

$12.60 |

$16.20 |

$233.00 |

|

|||

50-Year-Old Male |

$38.70 |

$72.00 |

$367.00 |

50-Year-Old Female |

$29.70 |

$51.30 |

$362.00 |

Cost calculated as of January 2025

Apply for a term life insurance policy with TD Insurance

Start by reviewing the TD Term Life Insurance plans and then get your life insurance quote. You can use the TD Life Insurance Calculator to help you determine how much coverage may be right for you. If you have questions, you can speak to a licensed life insurance advisor to learn more about your options.

Frequently asked questions

What is life insurance?

Life insurance is a contract between you and an insurance company, in which you agree to pay a premium. The life insurance policy can pay a lump-sum, tax-free amount, to a designated beneficiary when you pass away.

What is term life insurance?

A type of life insurance that provides coverage for a certain period and then expires. These plans have term periods within which premiums are guaranteed not to change.

Do I need individual term life insurance if I have group coverage?

Employer’s group term life insurance can be provided by companies as part of their employment benefits package. Individual term life insurance may be a good choice if you want a higher coverage amount than what is offered through your employer. For more information about the key differences between the two types of coverage, read our understanding employer's group term life insurance and individual term life insurance article.

What are the different types of life insurance plan options with TD Insurance?

10-Year Term Life

Could be suitable if you have short-term financial obligations such as a student or car loan, a mortgage, kids heading off to college or university, or you are approaching retirement.

20-Year Term Life

Could be suitable if you have longer-term financial responsibilities: you're newly married, have young children, or have recently purchased a home.

Term 100 Lifetime Coverage

Designed for those who want coverage that doesn’t expire after the insured reaches age of 80-years-old at a cost guaranteed not to increase. Could be suitable if you want to cover end of life expenses or leave a legacy to your loved ones, that could support them financially.

Guaranteed Acceptance Life Insurance

Offers guaranteed approval with no medical exam required for eligible applicants. Coverage can provide financial support to help your family pay for your final expenses, such as funeral costs, after your passing.

TD Term Life Insurance plans and TD Guaranteed Acceptance Life Insurance are individual life insurance plans underwritten by TD Life Insurance Company. Some restrictions may apply. Application subject to approval. See Insurance Policy(ies) for coverage details, including limitations and exclusions.

The content on this page is for general information purposes only and does not constitute legal, financial or insurance advice. Speak to a TD Life Insurance licensed professional advisor regarding your specific situation. The information contained herein, is subject to change without notice.

1World Health Organization 2024 data.who.int, Canada [Country overview]. (Accessed on 13 January 2025) data.who.int

2See Insurance Policy for definition of Canadian resident and other coverage details, including limitations and exclusions.

3The discount is only available to eligible applicants who apply for a new TD 10-Year or 20-Year Term Life Insurance policy using the online application. Offers cannot be combined with any other offer and is subject to change or may be withdrawn at any time.

4Cost calculated as of January 2025.

5Discounts are available to eligible applicants who are TD customers and apply for a new TD 10-Year or 20-Year Term Life Insurance policy. TD customer includes TD Auto Finance, TD Insurance Home and/or Auto and TD Wealth. Offers cannot be combined with any other offer and is subject to change or may be withdrawn at any time.

6The premiums shown are for illustrative purposes only. Your actual premium will depend on your individual circumstances and based on the information you provide during the application process.